Strategic Implications of the EU Market Integration Package on Crypto-Asset Service Provider Business Models and Revenue Architectures

- James Ross

- Dec 16, 2025

- 16 min read

1. Executive Summary:

1. The Macro-Strategic Shift: From “Move Fast” to Industrial Policy

The EU’s “Market Integration and Supervision” package (MiCA 2.0) represents a fundamental pivot from consumer protection to geopolitical industrial strategy. Grounded in the Draghi Report’s call to close the EU’s investment gap, this regulation aims to “sanitise” the crypto sector to mobilise household savings.

Strategic Implication: The era of “move fast and break things” is foreclosed. Digital assets are now treated as essential capital market infrastructure, requiring bank-grade compliance. Success will no longer be defined by user growth velocity, but by regulatory capital depth and integration with central bank rails.

2. Business Model Impact: The “ESMA Efficiency Frontier”

The centralisation of supervision under the European Securities and Markets Authority (ESMA) creates a regressive cost environment that renders the current small-cap “exchange” model obsolete.

“Big Bang” Centralisation: ESMA will directly supervise all CASPs, regardless of size. The regulation introduces a “Main Activity” test: even banks cannot hide crypto operations under their banking license if crypto operations exceed 50% of their turnover.1

The €15 Million Revenue Threshold: ESMA’s “Full Cost Recovery” model imposes high, fixed supervisory fees (minimum of €150k–€200k). Combined with the mandatory shift from compliance OpEx (personnel) to CapEx (institutional-grade ISO 20022 data infrastructure costing €2–3 million), the report projects an “Efficiency Frontier” of €15 million in annual revenue. Standalone firms below this line are structurally unviable.

Capital Intensity (Wind-Downs): A new “Orderly Wind-Down” mandate requires applicants to pre-capitalise their own liquidation before receiving a license. This significantly lowers Return on Equity (ROE) and acts as a massive barrier to entry.

3. Revenue Architecture: The “EMI Bridge” & Institutional Access

While compliance costs rise, the package unlocks significant revenue-growth opportunities by integrating crypto into the formal financial plumbing through the Settlement Finality Regulation (SFR).

The “EMI Bridge” Strategy: A standard CASP license is insufficient for direct access to central bank settlement rails (TARGET2). To bypass commercial banks and avoid “de-risking,” CASPs must upgrade to a “Dual-Structure” model by acquiring an E-Money Institution (EMI) license.

Cost: Requires ~€550,000+ in initial capital and distinct governance.

Revenue Driver: The EMI license doubles as a settlement key (margin efficiency) and a permit to issue Euro-stablecoins (EMTs), creating a high-margin yield generation stream.

Unlocking Institutional Capital: The SFR extends “finality” protection to DLT systems, legally immunising transactions from insolvency unwinding. This legal certainty is the prerequisite for Pension Funds and Insurance Companies to enter the market, unlocking a multi-trillion euro custody opportunity.

Vertical Integration (TSS): The permanent DLT Pilot Regime (cap raised to €100B) allows for a Trading and Settlement System (TSS) that combines exchange and CSD functions into a single entity.2 This allows crypto firms to offer near-zero clearing costs, competing directly with traditional exchanges.

4. Strategic Recommendations: 2025–2028

Firms must pivot from “retail speculation” models to “infrastructure” models to survive the transition.

Consolidation (M&A): Firms below the €15M revenue line must merge immediately to amortise fixed ESMA costs. Larger firms should aggressively acquire distressed entities holding EMI licenses to fast-track access to settlements.

Compliance-as-a-Service: Incumbents should commercialise their mandatory CapEx investments by white-labelling their regulatory infrastructure to smaller players and banks, turning a cost centre into a recurring revenue stream.

Treasury Pivot: Leverage SFR protections to build “Tri-Party Collateral Agents,” enabling corporate treasurers to use tokenised assets for repo transactions—moving the business model from retail trading fees to corporate cash management.

2. The Geopolitical and Economic Imperative: Contextualising the Reform

To truly understand the significance and scope of the “Market Integration and Supervision” package, it is essential to consider it beyond the framework of financial regulation. This package needs to be viewed within the larger context of the European Union’s geopolitical and macroeconomic strategy as it seeks to reverse a long-term decline in its relative economic power. While the initial draft appropriately referenced the Draghi and Letta reports, it failed to demonstrate how these documents serve as the foundational blueprints for the legislative text.

2.1 The Draghi Report and the “Investment Gap”

The current legislative momentum is influenced by the key findings from Mario Draghi’s September 2024 report, The Future of European Competitiveness. Draghi highlighted an annual “investment gap” of €750-800 billion needed to achieve the EU’s strategic goals in areas such as decarbonization, digitalisation, and defence. This amount represents about 4.5% of the EU’s GDP—an investment level not witnessed since the Marshall Plan.

The key insight for the digital asset industry is that the European banking sector, which has traditionally financed the European economy, is limited by capital requirements and risk aversion. It cannot fill this gap on its own. As a result, the European Commission views the development of deep, liquid, and integrated capital markets not as merely a desirable efficiency improvement, but as a geostrategic necessity. The regulation of the digital asset ecosystem is not intended to suppress it; instead, it aims to “sanitise” it, allowing it to facilitate significant capital mobilisation.

2.2 From Capital Markets Union (CMU) to Savings and Investments Union (SIU)

The rebranding of the Capital Markets Union (CMU) to the Savings and Investments Union (SIU) is more than a semantic shift; it represents a fundamental change in policy logic. While the CMU focused on the technical plumbing of cross-border trading, the SIU focuses on the source of funds: the €33 trillion in household savings primarily sitting in low-yield bank deposits.

The Commission’s strategy, clearly outlined in the March 2025 SIU communication, aims to unlock savings for productive assets, which is crucial for Crypto Asset Service Providers (CASPs). Under MiCA 1.0, crypto was seen mainly as a consumer protection issue. However, with the SIU framework (MiCA 2.0), crypto-assets, particularly tokenised securities and real-world assets (RWAs), are recognised as tools for wealth creation and industrial financing. This shift elevates their status and requires stringent compliance, integrating CASPs into the main Union’s financial framework.

2.3 The “Fifth Freedom” and the Failure of Soft Convergence

Enrico Letta’s April 2024 report, Much More Than a Market, argued that the Single Market’s four traditional freedoms (goods, services, capital, people) are insufficient for the 21st century. He proposed a “Fifth Freedom”: the freedom to research, innovate, and educate.

The legislative package addresses the issues caused by “soft convergence” that has led to fragmentation within the EU. For many years, the EU relied on directives, which require each member state to implement its own rules, alongside coordination among national regulators. This resulted in a landscape with 27 different “gold-plated” rulebooks, creating obstacles to cross-border innovation.

To resolve this, the shift to Regulations, which are directly applicable laws, and the establishment of centralised supervision by the European Securities and Markets Authority (ESMA) serve as the enforcement mechanisms for this initiative, known as the Fifth Freedom. The interpretation of purely national supervision as a non-tariff barrier to the free movement of capital and innovation underpins the significant transfer of sovereignty proposed in the Master Regulation.

3. The Supervisory Revolution: Anatomy of the Master Regulation

The primary focus of the legislative package is the proposal for a “Master Regulation” (COM(2025) 943). This comprehensive legal instrument amends nineteen existing regulations, including MiCA, MiFIR, and the ESMA Regulation. While the initial draft accurately identified the shift to the European Securities and Markets Authority (ESMA), it included significant ambiguities concerning the scope and mechanics of this transfer that need to be addressed.

3.1 Correction: The “Significant” vs. “All” CASP Paradigm

The initial draft expressed uncertainty regarding whether ESMA would supervise only significant CASPs (modelled on the ECB’s Single Supervisory Mechanism for banks) or all CASPs.

Fact-Check: The text of proposal COM(2025) 943 is explicit and uncompromising. The Commission has opted for a “Big Bang” centralisation. ESMA will become the direct supervisor for all CASPs authorised under MiCA, regardless of size.

This decision defies the tiered logic often seen in financial regulation. The Commission’s impact assessment concluded that a two-tier system would perpetuate regulatory arbitrage. In the crypto sector, an entity can scale from “insignificant” to “systemic” in a matter of months, moving faster than any national regulator’s re-designation process could manage. By supervising all entities directly, ESMA eliminates the “race to the bottom” where firms shop for the most lenient National Competent Authority (NCA).

The “Main Activity” Test:

The initial draft overlooked a critical exception. Traditional financial institutions, such as banks and investment firms, that offer cryptocurrency services as a secondary activity will generally continue to be supervised by their primary regulatory authority (like the European Central Bank or the national banking authority). However, the regulation introduces a “Main Activity” test: if crypto services constitute the entity’s “main activity”—defined as exceeding 50% of its turnover—then supervision will shift to the European Securities and Markets Authority (ESMA). This provision prevents crypto firms from obtaining a limited banking license merely to avoid oversight from ESMA.

3.2 The Mechanics of Transfer and the “Wind-Down” Mandate

The transition from national to supranational supervision is not immediate. The Master Regulation outlines a 24-month transition period following its entry into force.10 This interregnum creates a complex “shadow supervision” environment.

During this period, NCAs retain nominal authority but are legally bound to “cooperate” with ESMA on all authorisation decisions. This effectively means that CASPs applying for licenses must now satisfy two regulators: the local NCA (checking formal requirements) and the ESMA (checking business model sustainability and cross-border risks).

The Existential Threat of “Orderly Wind-Downs”:

An important detail missing from the initial draft is the strong position that ESMA has already taken on this transition. In its December 2025 statement on transitional measures, ESMA did not simply recommend caution; it explicitly directed National Competent Authorities (NCAs) to enforce “orderly wind-down plans” for any applicant that seems unlikely to meet the new, stringent ESMA standards by the transfer date.

This represents a significant change in regulatory approach. In the past, a rejected license application meant that a firm could not operate at all. Now, however, firms are required to pre-capitalise their own liquidation. They must maintain capital buffers sufficient to return all client funds and to close positions before they can obtain a full license. This new requirement significantly increases the business’s capital intensity, thereby reducing Return on Equity (ROE) and acting as a barrier to entry for self-funded startups.

3.3 Governance: The New Executive Board

To accommodate this expanded mandate, the Master Regulation establishes a new governance structure within ESMA, including an Executive Board composed of independent, full-time members. This board aims to protect supervisory decisions from the influence of national interests. Currently, ESMA’s Board of Supervisors consists of the heads of national regulators, who often advocate for their domestic industries. The new Executive Board removes this connection.

To accommodate this expanded mandate, the Master Regulation establishes a new governance structure within ESMA, including an Executive Board composed of independent, full-time members. This board aims to protect supervisory decisions from the influence of national interests. Currently, ESMA’s Board of Supervisors consists of the heads of national regulators, who often advocate for their domestic industries. The new Executive Board removes this connection.

4. The Economics of Compliance: Analysing the “Full Cost Recovery” Model

One of the most immediate threats to European CASPs’ Profit & Loss (P&L) statements is the harmonisation of fee-setting principles. The draft report correctly identified the “full cost recovery” model but overlooked its regressive impact on market structure.

4.1 The Unit Economics of Supranational Supervision

Under the proposed Regulation, ESMA is legally mandated to recover the full cost of its sector-specific activities from regulated entities. This differs structurally from many national regimes where supervision is partially subsidised by the state budget or fines collected from bad actors.

The cost stack for ESMA supervision is substantial. It includes:

Direct Personnel: Highly skilled specialists capable of auditing complex cryptographic systems.

Overhead: A proportional share of ESMA’s general administrative costs, HR, and the salaries of the new Executive Board.

SupTech Infrastructure: The amortisation of expensive IT systems required to monitor on-chain activity, ingest real-time transaction reports, and perform market surveillance across 27 member states.

The Regressive Impact of Fixed Fees:

While the regulation suggests fees will be allocated based on turnover, the administrative reality necessitates a significant minimum fixed fee to cover the baseline costs of supervising any entity, regardless of its size.

For a Large CASP: A supervisory fee of €2-3 million is a negligible fraction of revenue.

For a Small CASP: For an entity with €5-10 million in revenue, a minimum fee (e.g., €150,000-€200,000) represents a significant tax on gross margin, potentially pushing the entity into unprofitability.

This fee structure creates an “ESMA Efficiency Frontier.” We project that standalone CASPs with annual revenue under €15 million will become structurally unviable. They will be forced to consolidate to amortise these fixed supervisory costs over a larger revenue base.

4.2 Compliance as Capital Expenditure (CapEx)

The shift to ESMA supervision also fundamentally changes the nature of compliance spending. National regulators often accept periodic reporting in diverse formats. ESMA, by contrast, is a data-driven supervisor that mandates strict adherence to ISO standards (e.g., ISO 20022) and XML/XBRL submission formats for transaction reporting under MiFIR/MiCA.

This necessitates a shift from Operating Expense (OpEx)—hiring more compliance officers to check spreadsheets—to Capital Expense (CapEx), which is done manually. CASPs must build “regulatory APIs” and institutional-grade data warehouses capable of piping real-time order book and transaction data directly to ESMA’s central databases.

Strategic Implication: This requires a “bank-grade” data architecture. The initial capital outlay for this infrastructure is estimated at €2-3 million per entity. This favours well-capitalised incumbents and accelerates the exit of smaller players who cannot afford this upfront technology investment.

4.3 The “Gold-Plating” Paradox

The legislative package explicitly aims to reduce “gold-plating”—the practice of Member States adding extra requirements on top of EU rules.10 While this theoretically simplifies the landscape for cross-border firms, it creates a “levelling up” effect for firms currently domiciled in jurisdictions with “light-touch” implementation.

A CASP based in a jurisdiction that previously interpreted AML reporting requirements loosely will find ESMA’s interpretation of the EU baseline to be far stricter than their local regulator’s “gold-plated” version. Thus, “simplification” effectively means “intensification” for the majority of the market, removing the competitive advantage of domiciling in smaller, traditionally crypto-friendly member states.

5. The Settlement Finality Regulation (SFR): The Institutional Key

While the Master Regulation imposes costs, the proposal to convert the Settlement Finality Directive (SFD) into a directly applicable Regulation (SFR) (Proposal COM(2025) 941) offers the most significant revenue expansion opportunity. The draft report identified this but contained critical technical errors regarding access and eligibility that must be corrected to make the strategy viable.

5.1 Technological Neutrality: The “Bankruptcy Remote” Guarantee

The SFR explicitly extends “settlement finality” protection to systems based on Distributed Ledger Technology (DLT).

The Legal Innovation: The regulation codifies that a transfer order on a DLT system is “entered” and “irrevocable” at a specific moment defined by the system’s rules (e.g., block confirmation). Once this moment passes, the transaction is legally protected from being unwound by a liquidator or court, even if the participant subsequently goes bankrupt.

Commercial Value: This provides the legal certainty required for highly regulated institutional investors, such as Pension Funds and Insurance Companies, to trade on DLT venues. Without an SFR designation, these entities are effectively barred from holding tokenised assets due to the counterparty insolvency risk. This regulation unlocks the multi-trillion euro institutional custody market.

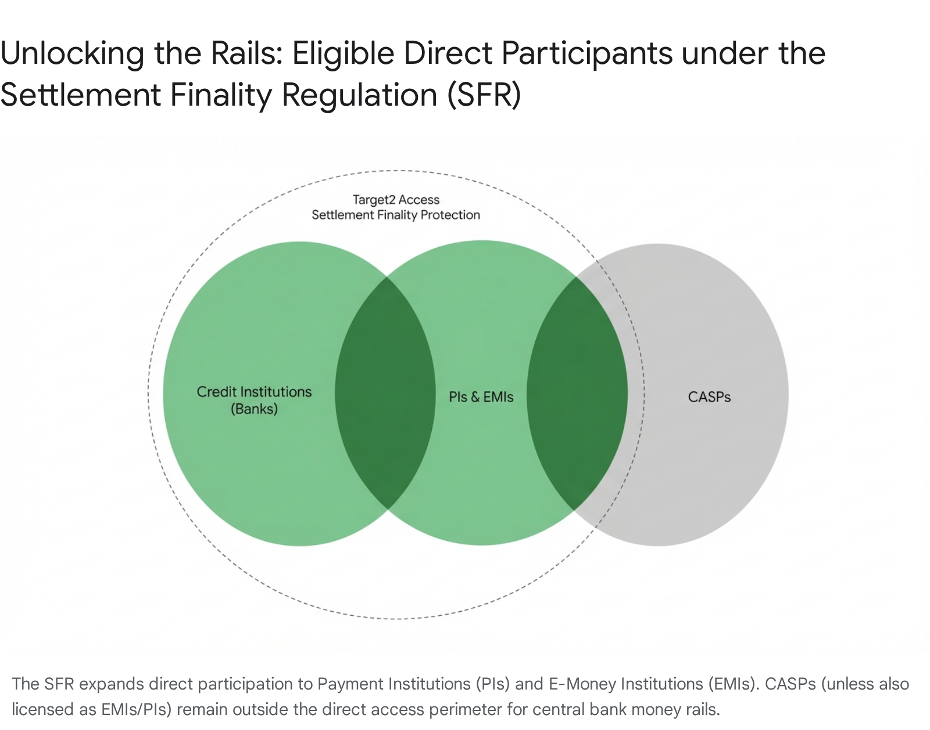

5.2 Direct Access: the “Participant” List

The SFR proposal expands the definition of “participant” to include Payment Institutions (PIs) and E-Money Institutions (EMIs).15 It does not explicitly list “CASPs” as a generic category eligible for direct participation in designated systems.

The Strategic Consequence: A standard CASP license is insufficient for direct access to central bank money settlement rails. To gain this access, a crypto group must either acquire or establish a subsidiary that is licensed as a Payment Institution or E-Money Institution.

The “Workaround”: Most major CASPs are already pursuing EMI licenses to issue E-Money Tokens (EMTs) under MiCA. The strategic value of these EMI licenses has now doubled: they are not just for issuing stablecoins, but also the key to accessing the Eurozone’s settlement backbone, allowing crypto firms to bypass commercial banks and settle directly in central bank money.

5.3 Redefining “Participants”: The Tiered Access Opportunity

The SFR also harmonises the rules for “indirect participation.” This creates a structured opportunity for CASPs who do not hold EMI licenses to act as “indirect participants” through a sponsoring bank or EMI. While less profitable than direct participation, it creates a legally recognised tier of access that was previously ambiguous.

The regulation clarifies that indirect participants must be disclosed and that their transactions can benefit from finality protections if certain conditions are met. This formalisation reduces the “de-risking” threat, where banks would arbitrarily cut off crypto clients, as a regulated access framework now governs the relationship.

5.4 The “EMI Bridge” Strategy

The European Commission’s proposal to convert the Settlement Finality Directive (SFD) into a directly applicable Regulation (SFR) creates a binary outcome for crypto-market participants. While it formally recognises DLT systems, it strictly limits direct access to central bank settlement rails (TARGET2/TIPS) to a closed list of “institutions.”

5.5 The Legal Gap: Why CASP ≠ Participant

Under the new Article 2(b) of the proposed SFR, the definition of a “participant” (entities eligible to settle directly in designated systems) has been expanded, but selectively.

License Type | SFR “Participant” Status? | Settlement Access | Strategic Consequence |

Credit Institution (Bank) | ✅ Yes | Direct | Full access to central bank money. |

Investment Firm | ✅ Yes | Direct | Limited by capital/system rules. |

Payment Institution (PI) | ✅ Yes | Direct | NEW: Can now access Rails directly. |

E-Money Institution (EMI) | ✅ Yes | Direct | NEW: Can now access Rails directly. |

Standard CASP (MiCA) | ❌ NO | Indirect Only | Must rely on a Bank/PI/EMI to settle fiat. |

The Risk: Without “Participant” status, a CASP remains operationally dependent on commercial banks. If the partner bank “de-risks” (terminates the account), the CASP loses its ability to instantly move fiat for clients.

5.6 The Strategy: The “EMI Bridge”

To secure operational independence and bankruptcy-remote finality, a CASP group must acquire or establish a subsidiary holding an EMI License. This “dual-structure” (CASP + EMI) acts as a bridge:

The CASP Entity: Handles crypto custody, execution, and matching (regulated under MiCA).

The EMI Subsidiary: Acts as the designated “Participant” in the settlement system and holds the central bank settlement account. It processes the fiat leg of the transaction directly.

5.7. The Cost of the Upgrade: CASP vs. EMI Requirements

Upgrading from a pure CASP to an EMI (under the incoming PSD3/PSR framework) requires a significant leap in capital and compliance infrastructure.

A. Capital Requirements (The “Cumulative” Trap)

Regulators (EBA) have indicated that capital requirements for hybrid Crypto/Payment entities are often cumulative rather than overlapping.

Standard CASP (Class 2/3):

Requirement: €125,000 – €150,000.

Focus: Operational risk, crypto-asset safeguarding.

EMI (under PSD3 Proposal):

Requirement: €400,000 (increased from €350k under EMD2).

Focus: Liquidity risk, float management.

Total Capital Injection: A CASP upgrading to this model effectively requires ~€ 550,000 in initial capital, plus distinct “Own Funds” buffers calculated against transaction volume (Method D).

B. Safeguarding & Governance

Safeguarding: An EMI must ring-fence client funds. Unlike a CASP (which can sometimes use a broader range of custodians), an EMI must hold 100% of client float in secure, low-risk liquid assets or a segregated account at a Credit Institution or Central Bank.

Governance: The EMI subsidiary requires a dedicated Board of Directors and specialised “Heads of Function” (Compliance, Risk, Internal Audit) that are distinct from the CASP’s management to avoid conflicts of interest.

5.8 Strategic ROI: Why Pay the Premium?

Despite the higher capital costs (€400k+ vs €150k), the EMI license offers three specific ROI drivers under the SFR:

Settlement Finality Protection:Transactions routed through your EMI subsidiary are covered by Article 3 of the SFR. Once the “moment of entry” passes, the fiat transfer is legally irrevocable. This allows you to offer institutional clients (Pension Funds) a guarantee that their settlements cannot be unwound by a liquidator—a prerequisite for their entry into the market.

Margin Efficiency:By settling directly in Central Bank Money (or commercial bank money via your own rail access), you eliminate the correspondent banking fees and t+1 delays typically charged by sponsor banks.

Stablecoin Issuance (EMT):The EMI license is required under MiCA to issue E-Money Tokens (EMTs). This license, therefore, kills two birds with one stone: it grants access to settlement rails and permits the issuance of a compliant Euro-stablecoin.

6. DLT Pilot Regime 2.0: The Permanent Sandbox

The legislative package includes targeted amendments to the DLT Pilot Regime to address the flaws that hampered its initial uptake. The draft report correctly identified the lifting of thresholds but missed the strategic significance of the “Permanent Status”.

6.1 From Experiment to Market Structure

The proposal removes the “sunset clause” of the DLT Pilot Regime.17 This signals to the market that DLT is no longer a “test” but a permanent, parallel track of the EU financial landscape.

Threshold Increase: The aggregate market capitalisation cap for DLT Market Infrastructures (DLT MIs) is raised from €6 billion to €100 billion.11 This is a game-changer. It allows the issuance of “benchmark-sized” corporate bonds and even sovereign debt on-chain, activities previously impossible due to the low cap.

The “TSS” Advantage: The Pilot Regime allows for a Trading and Settlement System (TSS)—a combined exchange and CSD within a single legal entity.19 This vertical integration is prohibited in traditional finance (where trading and settlement must be unbundled).

Strategic Pivot: This regulatory privilege gives DLT MIs a structural cost advantage. By eliminating the need for reconciliation between separate exchange and CSD ledgers, a TSS can offer near-zero clearing costs and atomic settlement. We predict that traditional exchanges (Euronext, Deutsche Börse) will now aggressively migrate segments of their ETF and small-cap equity markets to DLT TSS structures to capture these efficiency gains, placing them in direct competition with crypto-native firms.

7. The Pan-European Market Operator (PEMO) and Corporate Strategy

The PEMO status is primarily designed for traditional stock exchange groups (like Euronext or Nasdaq) to operate multiple national trading venues under a single license and supervisor. However, the legislation is drafted in a way that creates a powerful precedent for large, cross-border CASPs.

A CASP authorised by the ESMA under the new Master Regulation is essentially a PEMO for the crypto asset class. It operates across all 27 member states under a single license and a single supervisor. The “PEMO” label in the regulation validates the “group supervision” model that crypto firms have long advocated for. It allows them to centralise liquidity pools that were previously fragmented by national ring-fencing rules.

Strategic Implication: This incentivises the formation of large, pan-European crypto groups. We expect to see:

Horizontal Consolidation: Large CASPs acquiring regional competitors not just for their user base, but to migrate them onto the central “PEMO-like” license, shutting down the redundant national entities and saving on compliance costs.

Vertical Integration: CASPs acquiring custodians or technology providers to own the entire value chain from execution to settlement, leveraging the TSS model in the Pilot Regime.

8. Strategic Recommendations: The Pivot to “Infrastructure”

Based on the corrected analysis of the package, the following strategic pivots are recommended for CASPs seeking to survive the consolidation wave:

8.1 The “SaaS” Pivot (Compliance-as-a-Service)

The high fixed costs of ESMA compliance will crush smaller players. Large, well-capitalised CASPs should treat their compliance infrastructure not as a cost centre, but as a product. By building institutional-grade RegTech (regulatory technology) reporting and surveillance engines, they can white-label this infrastructure to smaller firms, banks entering the crypto space, or even traditional asset managers. Selling “Compliance-as-a-Service” creates a high-margin, recurring revenue stream that helps offset the new supervisory fees.

8.2 The “Treasury” Pivot (Collateral Management)

With the SFR providing legal certainty, CASPs should move beyond retail trading fees and build “Tri-Party Collateral Agents” on DLT. They can offer services that enable corporate treasurers to use tokenised Money Market Funds (MMFs) or stablecoins as intraday collateral for repo transactions. This integrates crypto into the €10 trillion European repo market, moving the business model from “retail speculation” to “corporate cash management” and “treasury optimisation.”

8.3 The “Consolidation” Pivot (M&A Strategy)

Firms must immediately assess their revenue against the “ESMA Efficiency Frontier” (estimated at €15M annual revenue).

Firms below this line: Must seek a merger partner immediately to achieve scale before the transition period ends.

Firms above this line: Should prepare war chests to acquire distressed competitors. The strategy should target smaller firms that hold valuable EMI licenses. Acquiring an EMI is the fastest route to unlocking direct settlement access under the new SFR. This capability will be a decisive competitive advantage in the institutional market.

9. Conclusion

The “Market Integration and Supervision” package signifies the conclusion of a turbulent period in the cryptocurrency sector. By centralising oversight, standardising fees, and establishing firm settlement finality, the European Commission has created a robust regulatory framework. While operating within this framework may involve high costs, it provides guaranteed legal certainty. Conversely, businesses operating outside this system face challenges to their viability.

In this new era, success will not necessarily belong to firms with the best marketing strategies or the lowest trading fees. Instead, the winners will be those with the most substantial regulatory capital, the most efficient compliance infrastructures, and well-integrated post-trade operations. The age of the “Crypto Exchange” has come to an end; we have now entered the era of “Digital Asset Market Infrastructure.”

#DigitalAssets #MarketStructure #ESMA #MiCA2 #SettlementFinality #IndustrialPolicy #InstitutionalCrypto